As a consumer with a bad or no credit history, you may find it challenging to access loans and other financial products through traditional means. No-credit-check loans could seem like an appealing option when you have an urgent need for cash and limited alternatives. However, these loans come with significant risks that you must weigh carefully before proceeding.

What Are No Credit Check Loans?

No credit check loans are unsecured personal loans that don’t require a credit check. They allow you to borrow money without going through a traditional credit check. These loans are ideal if you have bad credit or no credit history. However, they often come with higher interest rates to offset the lender’s risk. The renowned broker WeLoans has listed the 10 best no credit check loans for your potential needs.

The main benefits of no credit check loans are:

- Access to emergency funds even with bad credit. No credit check loans provide access to quick cash when you have urgent financial needs but can’t qualify for other loans.

- Opportunity to build credit. If you make on-time payments, no credit check loans can help establish or rebuild your credit history over time.

The potential downsides to consider include:

- Higher interest rates. Lenders charge higher rates due to the increased risk of lending to borrowers with poor or no credit. Interest charges can accumulate quickly if not repaid fast.

- Chance of getting scammed. Some predatory lenders target people with bad credit. Make sure the lender is reputable and the terms are fair before signing anything.

- Debt cycle. The high interest rates can make these loans difficult to pay off and you may need to take out new loans to pay off previous ones. This can lead to a vicious debt cycle.

- Limited regulation. No credit check loans are not as regulated as regular personal loans. Lenders can charge excessive fees and interest rates. Read the fine print carefully.

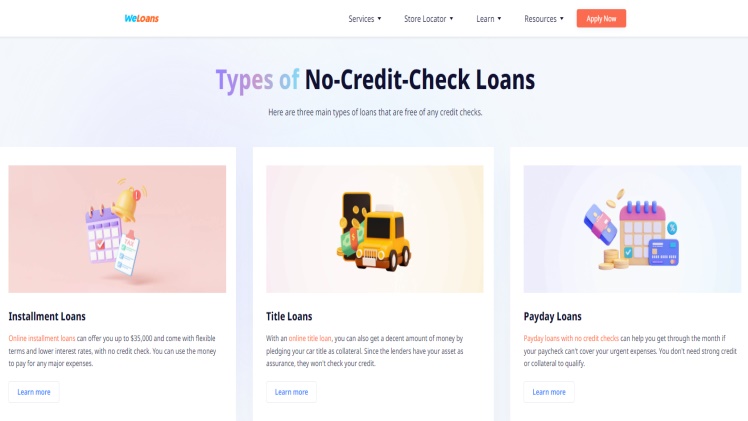

Types of No Credit Check Loans: Payday Loans, Personal Installment Loans, Etc.

No credit check loans from WeLoans’ source allow you to borrow money without undergoing a traditional credit check. While convenient, these loans often come with high interest rates and fees. The types of no credit check loans include:

- Payday loans: Small, short-term loans that must be repaid with your next paycheck. Payday loans typically have very high annual percentage rates (APRs), sometimes over 300%. Only use payday loans for emergencies and if you can pay the loan back quickly.

- Personal installment loans: Loans that are repaid over fixed monthly payments. Installment loans usually have lower APRs than payday loans but higher than credit cards or personal loans from banks. Only borrow what you can afford to pay back to avoid getting caught in a cycle of debt.

- Title loans: Loans secured using your vehicle title as collateral. Title loans have very high APRs, often over 300%, and you risk losing your vehicle if unable to repay the loan. Only use title loans as an absolute last resort in an emergency.

Benefits of No Credit Check Loans

Convenient Access to Funds

WeLoans has no credit check loans that provide quick access to cash when you need it most. Since your credit history is not reviewed, the application process is streamlined and funds can be deposited directly into your bank account within a day or two after approval. This can be helpful in emergency situations or to cover unexpected expenses that arise between paychecks.

No Credit Score Impact

Applying for a no credit check loan will not negatively impact your credit score or credit history. Since your credit is not pulled, there is no hard inquiry on your credit report. Your credit score remains unchanged, which can be important if you’re working to build or rebuild your credit.

Various Loan Types Available

There are several kinds of no credit check loans to choose from depending on your needs:

- Payday loans: Short-term loans (usually 2 weeks) with high interest rates. Funds are repaid on your next payday.

- Installment loans: Longer-term loans (3 months to 2 years) with fixed repayment schedules. Interest rates are often lower than payday loans.

3.Line of credit: Provides access to funds as needed up to a certain limit. You only pay interest on the amount borrowed. Can be revolving.

4.Title loans: Uses your vehicle title as collateral. Typically must be repaid within 30 days to avoid losing your vehicle. Risky and often predatory.

Potential Downsides to Consider

While no-credit-check loans may seem appealing due to their accessibility, there are some significant downsides to consider before taking one out.

Higher Interest Rates

Since the lender is taking on more risk by not checking your credit, the interest rates for no-credit-check loans are typically much higher than average. The higher rate is to offset the increased chance of default. Interest rates can be over 36% APR, which costs thousands more over the life of the loan.

Shorter Repayment Terms

No-credit-check loans often come with very short repayment terms, sometimes only 2 to 5 years. The short timeframe, combined with a high interest rate, means your payments will be quite high, potentially difficult to keep up with. If you can’t pay the loan off quickly, the total interest paid can end up being more than the original loan amount.

Fees and Penalties

In addition to high interest rates, no-credit-check lenders frequently charge various fees like origination fees, application fees, and late payment penalties. These additional fees increase the overall cost and can make getting out of debt even harder. Late or missed payments also negatively impact your credit score.

Limited Borrowing Amount

No-credit-check loans typically only lend a few hundred to a few thousand dollars at most. The small amounts, while more accessible, may not suit larger financial needs. If you need more substantial funding, a no-credit-check loan is probably not the right option.

Potential Fraud

Some predatory lenders market no-credit-check loans but have hidden fees, extremely high-interest rates, or fraudulent terms. Do extensive research on any lender before taking out a loan to avoid becoming a victim of fraud or predatory lending practices. Legitimate lenders will clearly disclose all rates, fees, and terms upfront.

Are No Credit Check Loans Right for You? How to Decide

To determine if a no-credit-check loan is right for your needs, evaluate the pros and cons and how they apply to your unique financial situation.

Pros

- Quick access to funds. No-credit-check loans provide fast approval and funding since there is no credit check. The money can be deposited in your account within a day or two.

- Few eligibility requirements. As long as you have a steady income and a bank account, you have a good chance of qualifying.

- Can help rebuild credit. Some lenders report payments to credit bureaus, which can help you establish or rebuild your credit history over time if you make on-time payments.

Cons

- High interest rates. Lenders view no-credit-check loans as risky, so interest rates are often very high, sometimes over 36% APR. This can make the loans difficult to repay.

- Low loan amounts. No-credit-check loans typically only provide a few hundred to a few thousand dollars. The amounts are too small for many financial needs.

- Risk of predatory lending. Some no-credit-check lenders engage in predatory practices like aggressive marketing, hidden fees, and making unrealistic promises. Be very cautious.

- Can damage credit if mismanaged. Late or missed payments can further damage your credit and lead to collection calls, lawsuits, and wage garnishment.

Types of No-Credit-Check Loans

- Payday loans: Small, short-term loans (usually $500 or less) that must be repaid in full with your next paycheck. Interest rates are extremely high.

- Installment loans: Slightly larger amounts ($1,000-$5,000) repaid over 6-36 months. More affordable but still have high rates.

- Title loans: Use your vehicle title as collateral for a loan, usually 25-50% of the vehicle’s value. If unable to repay, you risk losing your vehicle.

Conclusion

In summary, no-credit-check loans may seem appealing if you have a poor credit score or no credit history and need quick access to funds. However, the high interest rates and strict repayment terms often mean this type of financing should only be used as an absolute last resort. Before you sign on the dotted line, make sure you understand all the details and can truly afford the payments.